What are Prescription Drug Plans?

Prescription Drug Plans (aka Part D) offer insurance coverage solely for prescription drugs. They DO NOT cover over-the-counter drugs, compounded drugs, or holistic medicines. For most states there are over 10 Prescription Drug Plans available and they are sold by a myriad of private insurance companies.

Is purchasing a Prescription Drug Plan required?

Medicare rules stipulate that you must have “credible prescription drug coverage” when your turn 65. If you don’t, you will be assessed a penalty at the time you do obtain this coverage. This penalty is called a Late Enrollment Penalty (LEP) and it is added to the monthly premium of your drug plan. Click here for more information on Late Enrollment Penalties.

“Credible prescription drug coverage” can present itself in many forms. You don’t have to have a private, stand-alone prescription drug plan in order to have coverage that is considered credible. In fact, there are several types of drug coverage that qualify as credible coverage with Medicare. Here is a list of the most common types:

- Employer coverage

- VA benefits

- Medicare Advantage Prescription Drug plan (MAPD)

- Stand-alone Prescription Drug Plan

- Former employer retiree plans

However, just because you have one of these types of coverage does NOT guarantee the coverage is credible. We highly recommend you consult your employer’s Human Resources Department, your insurance agent, or the Office of Veteran’s Affairs to confirm your coverage qualifies.

How do I pick a drug plan?

Easy question, complicated answer. With so many plans to choose from, selecting the right one can be daunting. And, there are different ways to tackle this. Some choose a plan offered by a carrier they are loyal to. Others pick the cheapest plan.

At Sovereign Seniors LLC, we take a practical and customized approach to recommend the drug plan that will cover all your drugs and save you the most money. To do this, we gather pertinent information about the drugs you take, the strength of each prescription, the pharmacies you prefer, the frequency you fill each prescription, and your preferred way of filling your prescriptions. This information is used in tandem with the Medicare.gov website to evaluate each plan’s ability to meet your needs. Contact us for a free review of your prescription drug coverage and for help selecting a plan.

How much do plans cost?

Because there are numerous Prescription Drug Plans available in any give state, there is no straight answer to this question. Premiums vary significantly. The Center for Medicare and Medicaid Services (CMS), however, has shared that the national average for a Part Drug plan premiium in 2026 is $38.99. If you are trying to budget this monthly cost, this is a good number to use.

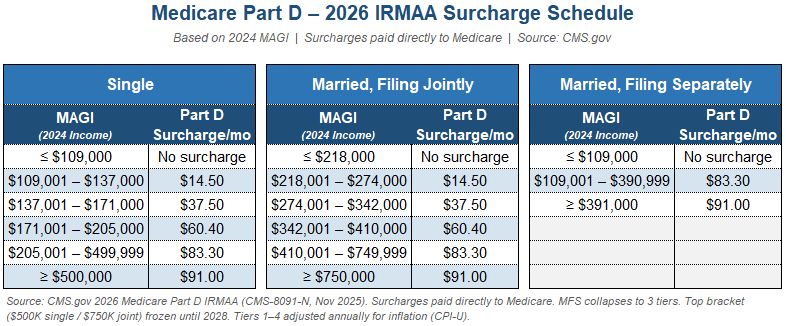

It is possible your premium will be higher than the base amount quoted by your carrier. Just like with your Original Medicare Part B premium, high wage earners will be assessed an Income Related Monthly Adjustment Amount (IRMAA) if your modified adjusted gross income (MAGI) on your tax return from two years ago exceeds certain thresholds. The chart below indicates how much extra you will pay if you are assessed an IRMAA in 2026.

What are “Coverage Stages”?

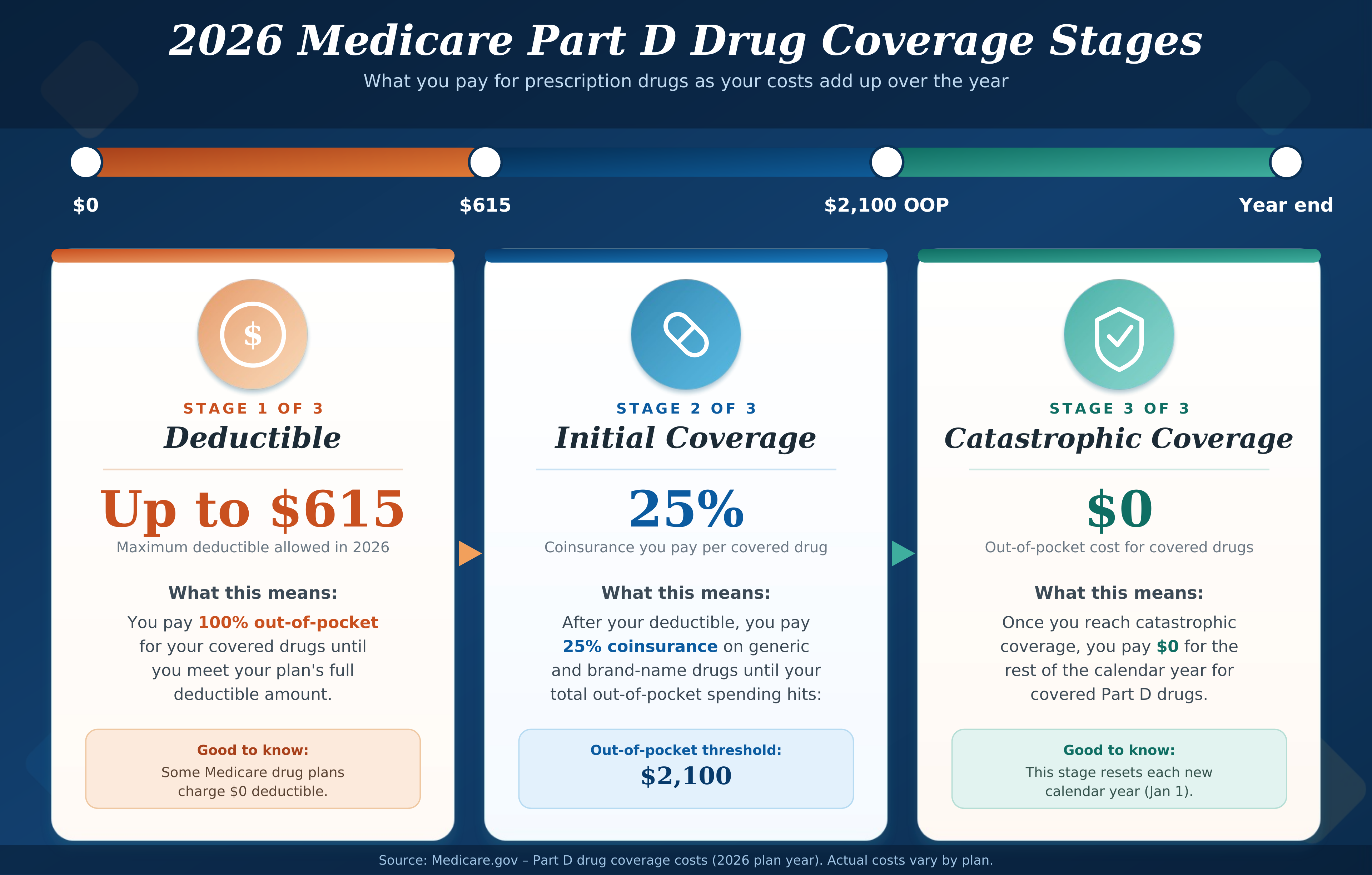

In a nutshell, this is the best way we can think of to simplify a complicated topic: The price you are paying to fill a prescription drug at the pharmacy might not remain the same throughout the year. Why? Because the price you pay for your drugs depends on what “Coverage Stage” you are currently in. Take a look below to learn more about these three stages.

The difference between these three stages is how much you pay for your prescriptions. These amounts are noted in bold on the chart above. You begin the year paying toward your deductible (Stage 1) and will pay 100% of your drug costs until you reach the standard annual deductible which, in 2026, is $615. Once the deductible is met, you move to the Initial Coverage Stage (Stage 2).

In Stage 2 drug coverage, you pay 25% of the cost for each drug you fill. For many prescriptions, this is a price decrease from what you were paying in Stage 1. You will pay this new amount for each drug you fill until your Total Out-Of-Pocket Threshold is met. What is that you say? Your Total Out-Of-Pocket Threshold (aka TROOP) is the total amount that you and any other entities (like your drug plan policy, Medicare, or drug manufacturers) pay on your behalf for your drugs. The threshold maximum for 2026 is $2,100 and, once you reach that, you move to Catastrophic Coverage (Stage 3).

In our experience, about 35% of client reach the Catastrophic Coverage stage each year. Should you make it to this stage, you are done paying for your prescription drugs through the end of the calendar year. The first of each year, this three-stage progression starts over. For more information regarding this process, click here.

How can I reduce my drug costs?

The high costs of prescription drugs is a hot topic…in communities across the country as well as with our politicians in Washington D.C. Here are a few current ways to reduce the cost of your prescription drugs:

- If you have limited resources, the Social Security Administration offers a program called Low Income Subsidy (LIS) or Extra Help. To qualify for this program, your income and savings needs to fall within certain ranges. To learn more or see if you qualify, click here.

- GoodRx. This website offers free coupons and searches for the lowest local prices on your drugs. They offer a discount card which you present at the pharmacy when paying. While this program offers tremendous relief to thousands, there are a few things to note for Medicare beneficiaries:

- If your insurance coverage details are already stored in your pharmacy’s system, it’s possible they will not accept your GoodRx card or honor the discount.

- The price you pay on prescriptions using GoodRx will not apply to your deductible.

- This –and all–pharmacy discount plans DO NOT qualify as credible prescription drug coverage. You will still need to have credible prescription drug coverage in order to avoid Medicare’s Late Enrollment Penalty.

- Contact the pharmaceutical company. Most pharmaceutical companies offer cost-relief programs (or coupons at a minimum).